Also referred to as an ARM, an adjustable rate mortgage is a type of home loan where the property being bought is utilized as security. This differs from a fixed-rate mortgage, which locks in your interest rate for the duration of the loan. Conversely, an ARM offers a stable rate during a preliminary period that usually ranges from three to ten years; after this time, the rate can increase or decrease.

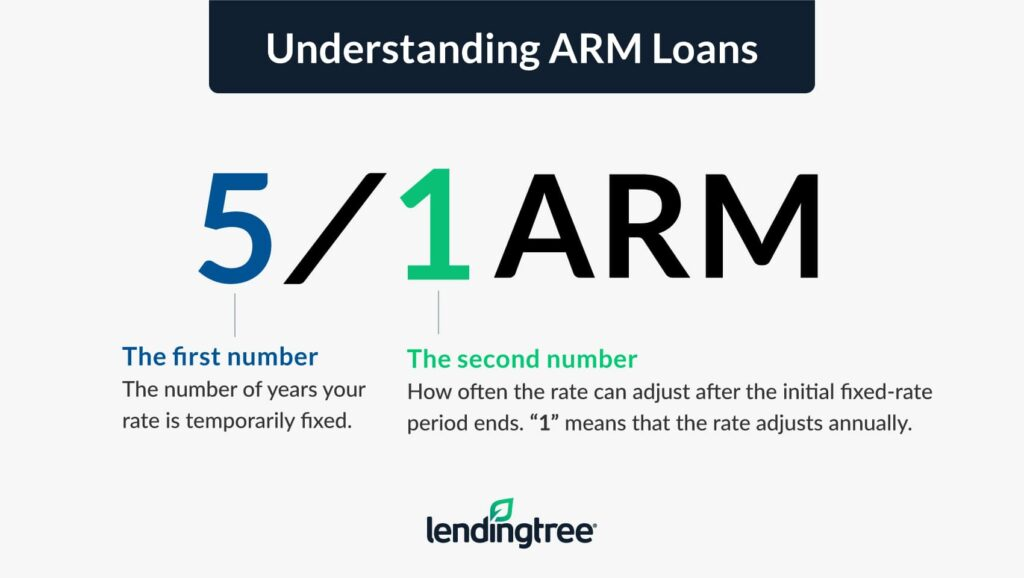

An example of this would be a 3/1 ARM, where your interest rate remains steady for the first three years before adjusting each year for the remaining 27, given a standard 30-year loan term. Other common types include 5/1, 7/1, and 10/1 ARMs.

Because the initial interest rates for ARMs are typically lower than those for fixed-rate mortgages, their monthly payments are often less. However, if interest rates significantly rise during the loan’s term, this can change.

An ARM might be a suitable choice under certain conditions:

- You anticipate that interest rates will decline in subsequent years.

- You plan on refinancing prior to the end of the introductory period.

- You foresee a future income increase that could balance potential higher payments.

- You intend to sell your home before the initial interest rate goes up.

Alternatively, it might be best to steer clear from an ARM if:

- You prefer to avoid financial risks.

- There is uncertainty about your income level increasing in the future.